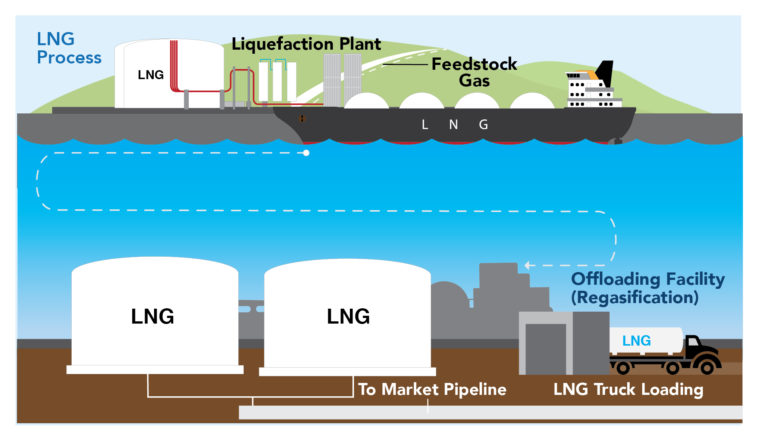

Liquefied Natural Gas (LNG) represents a pivotal innovation in the global energy landscape, offering a versatile and efficient solution for the transportation and storage of natural gas. By cooling natural gas to approximately -162°C (-260°F), it transforms into a liquid state, significantly reducing its volume by roughly 600 times; facilitating cost-effective international trade and enabling access to remote markets. This technological advancement has bolstered energy security, diversified supply chains, and contributed to the global transition towards cleaner fuel alternatives.

Source: Center for LNG

As demand for LNG continues to surge, driven by environmental policies and the quest for lower-carbon energy sources, the industry is evolving with advancements in liquefaction, regasification, and shipping infrastructure, ensuring its role as a cornerstone of the modern energy economy.

The global liquefied natural gas market size was valued at USD 122.60 billion in 2024 and is expected to witness a CAGR of 11.6% from 2025 to 2030 to reach USD 226.97 billion by 2030.

Source: Global LNG Hub Market Analysis and Insights

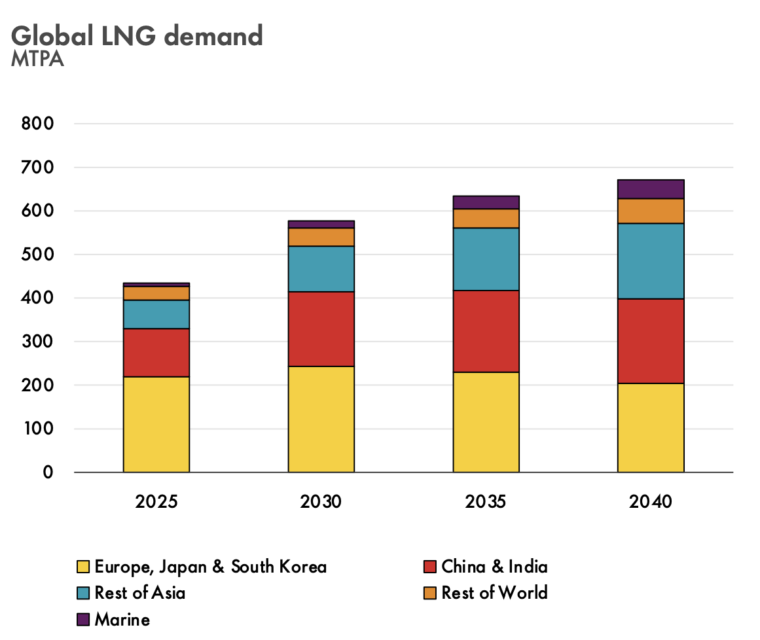

The global LNG market has expanded significantly, driven by high demand in the Asia-Pacific region as they seek to diversify their energy mixes and enhance energy security. To meet the demand, China is enhancing its LNG infrastructure, with expansions in Guangdong, Guangxi, and Hainan provinces. India’s natural gas consumption is projected to rise by 60% to 103 billion cubic meters annually by 2030, driven by urbanization and industrialization, with domestic production growing only 8%, doubling LNG imports to 65 billion cubic meters, while the government expands LNG infrastructure and secures long-term contracts. Additionally, emerging markets such as Vietnam, Philippines and several African nations are anticipated to become new importers, driven by increasing energy needs and infrastructure developments. In contrast, Europe’s LNG demand is expected to peak by 2025 and decline through 2030, influenced by high prices, energy security mandates, and climate policies. Lastly, Japan, traditionally a leading LNG importer, may experience stable or slightly reduced demand due to energy diversification efforts and a focus on renewable energy sources.

Source: Institute for Energy Economics and Financial Analysis

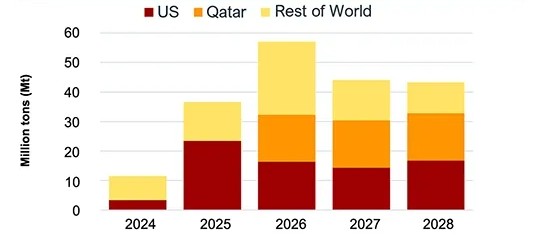

On the supply side, substantial expansions are underway to meet this growing demand. The United States is expected to account for 29% of the global LNG supply by 2030, positioning itself as a leading exporter. Qatar is also significantly boosting its production capacity through the North Field Expansion project, aiming to increase LNG output by over 60% by 2027. Additionally, countries like Canada and Mexico are investing heavily in LNG export infrastructure to cater to Asian markets, with projects such as LNG Canada and Sempra’s Energia Costa Azul LNG expected to commence operations in 2025. Australia is expected to maintain a significant share of the LNG trade with existing partners over the medium term, owing to established trade relationships and its proximity to Asia. These developments indicate a robust global LNG supply landscape, with major contributions from North America and the Middle East anticipated during this period.

Source: Bloomberg Finance L.P.

Global LNG prices have experienced significant fluctuations in recent years, influenced by various factors. In February 2025, the European benchmark Dutch Title Transfer Facility (TTF) averaged $15.28 per million British thermal units (MMBtu), while Asia’s Japan Korea Markert (JKM) averaged $14.40 per MMBtu. These price variations are driven by factors such as supply-demand imbalances, geopolitical tensions, seasonal weather patterns (LNG demand increases in cold weather as it’s residential uses are for cooking, heating homes and generating electricity), and the availability of alternative energy sources. For example, increased U.S. LNG exports to Europe during colder months have impacted global prices. Additionally, the expansion of LNG production capacities in countries like Australia and Qatar has influenced global supply dynamics, contributing to price volatility. Recently, with the start of the Trump Administration, numerous Asian countries, namely – Japan, India, Taiwan, and Bangladesh, have expressed interest in buying US LNG to fend off tariffs, diversify supplies, and narrow trade deficits with the US.

Thus, balancing the anticipated demand surge with sustainable pricing and supply stability remains a critical focus for the LNG industry in the coming years.